As we enter 2024 and hoteliers gear up to execute their plans for the coming year, it’s important to reflect on the trends and developments that have shaped the industry over the past year.

As we enter 2024 and hoteliers gear up to execute their plans for the coming year, it’s important to reflect on the trends and developments that have shaped the industry over the past year.

Despite some lingering concerns around the broader economy and geo-political instability, we can confidently say that travel has fully recovered in 2023.

While obstacles still remain and will continue to rise, we can look back on 2023 and forward in 2024 with optimism and recognize the potential for growth and innovation.

Here are our key learnings from 2023.

Despite tougher conditions, consumers kept spending on travel

In 2022, it was pretty much a given that we were going to see a big travel and tourism rebound given the artificially depressed years of travel restrictions that had preceded it.

One year later and that surety was falling away as high inflation ate away at consumer spending power, as did rapid rises in interest rates to counter those soaring prices. There was now a global crunch in discretionary spending, and many economists warned about the impact to livelihoods and even the potential for a global recession.

Fast forward to the close of the year, and travelers decisively defied the gloom. Global expenditure on travel and tourism has remained incredibly robust even in the face of weakening household spending power.

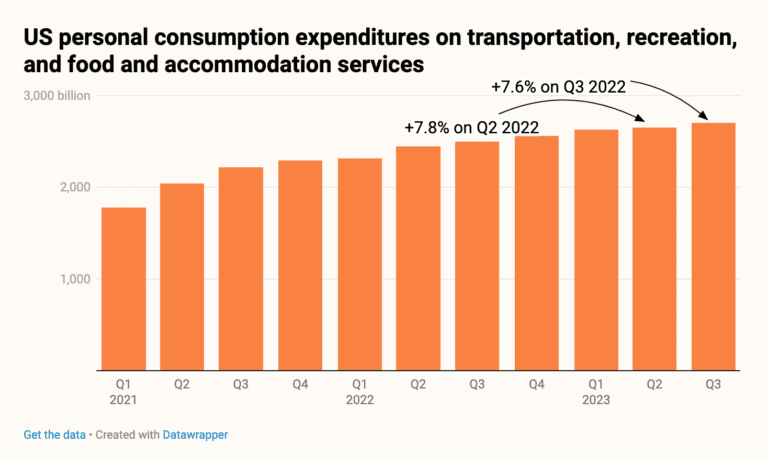

In the US, which opened up earlier than other economies and had very high rates of growth in the travel sector in 2022, momentum continued in 2023. While the previously explosive rates of growth have come down, US consumers still spent 8% more on transportation, recreation, and food and accommodation services than a year prior in both Q2 and Q3 2023.

Even in less robust economies where consumer discretionary spending has been squeezed more than in the US, there seemed to be little let up in the desire to book trips. While Japanese households cut overall spending by the highest amount in nearly two-and-a-half years in Q2 2023, they continued to increase the amount of their budgets going towards dining out, transportation, culture and entertainment services.

Similarly, Barclays’ October UK Consumer Spending Report noted that the travel sector “continues to be one of the best-performing categories of 2023,” with spending rising 10.5% in October 2023, even amid a cost of living crisis.

In 2023, the desire to see the world could not be dampened.

Events remain a huge demand driver for hotel and short-term rental bookings, while business travel provides a welcome boost

One of the main drivers for this continued spending by consumers and the overall strength in the travel and tourism sector seems to be the drive to experience things in person and reject the online world forced upon us due to the pandemic.

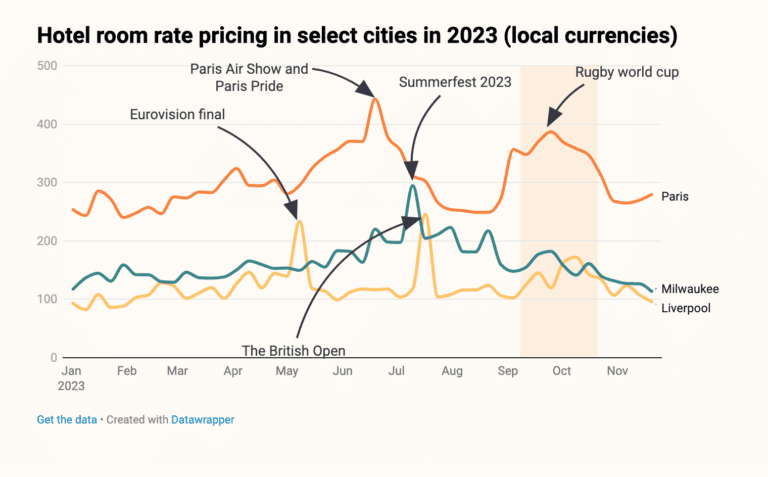

Whether it was Primavera and Sonar festivals in Barcelona, Eurovision in Liverpool, Summerfest in Milwaukee, the Rugby World Cup in Paris, Taylor Swift’s Eras Tour, or the Women’s World Cup down under in Australia and New Zealand, excited fans turned out in droves for major sporting, cultural and music events.

Just by glancing at the chart for some of these cities mentioned above, there are clear spikes in hotel room pricing where those events fell in the calendar for their respective cities, which are marked in the chart.

Those boosts to room rates underlined the strong demand generated and the subsequent capacity for hoteliers to set higher rates in all of those cases.

People weren’t only traveling for pleasure, though, as the personal touch very much returned to business travel as well.

Business travel expenditures, previously expected to be one of the slowest recovering aspects of the economy post-COVID, are now rapidly approaching where they were in 2019.

The October 2023 GBTA Business Travel Outlook Poll reported that 84% of respondents considered that their company’s business travel in 2023 had recovered to near-2019 levels, while the Global Business Travel Association (GBTA) has repeatedly revised up its projections so that it now expects 2023 spend to be roughly comparable to 2019.

Indeed, according to the Knowland and Amadeus Hospitality Group & Business Performance Index (HGBPI), group business in the US is now above where it was in 2019, while for the year up to Q3, the volume of hosted events had reached 91% of the pre-pandemic level.

There appeared to be no diminishing of enthusiasm for the experience economy going forward either, as rates and bookings for major events, such as the Paris Olympics or Euro 2024 football tournament, are extremely high, even for such high-profile events. While the GBTA predicts that business travel spending will exceed 2019 levels in 2024.

The Chinese travel market is slow to wake for outbound destinations

Back in April 2023 we dove into our data and predicted that the Chinese market was going to be something of a slow grower, likely missing the expectations of hopeful tourism bodies hungry for high-spending Chinese tourists.

So, what happened?

Well, the data doesn’t lie, and while Chinese tourists have been venturing back outside the Middle Kingdom, they are doing so in much smaller numbers than the more bullish forecasts had hoped.

Previous hotspots, like Japan, Thailand and South Korea have found themselves with big shortfalls in arrivals versus their expectations at the start of the year, and it seems likely that this underperformance will continue into next year.

For example, you would need to go back a decade to find comparable numbers for mainland Chinese visitors to Japan in the year to August 2023, whereas Thailand welcomed 2.8 million visitors in the year to October 2023, which would put it way behind its initial target of 5 million visitors from the country.

That doesn’t mean that the Chinese consumer has lost interest in travel, but that the response to COVID in China has resulted in behavioral changes. Many more Chinese travelers are looking at internal destinations.

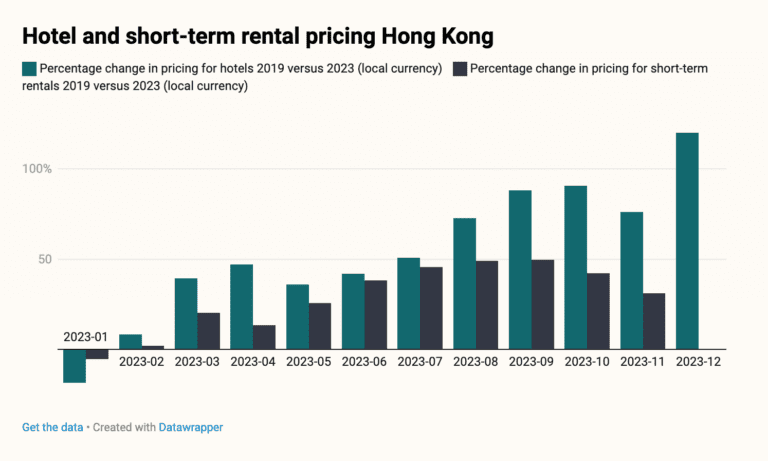

The 2023 Golden Week holiday resulted in record train and air travel numbers, and many have returned to perennial favorites Macau and Hong Kong. Hong Kong illustrates this point well. There were steady rises in pricing for hotels and short-term rentals throughout the year when compared to 2019, particularly for the former.

As we approach a key travel period for the Chinese market to close 2023, rates for a standard hotel room in Hong Kong for December had more than doubled as of the time of writing, being priced 120% above 2019.

As we approach a key travel period for the Chinese market to close 2023, rates for a standard hotel room in Hong Kong for December had more than doubled as of the time of writing, being priced 120% above 2019.

There seems little reason to expect these dynamics to drastically change either in 2024, with modest growth in outbound tourism and greater focus on the internal market from Chinese travelers.

China’s civil aviation authority winter and spring flight plans proudly announced 34% more scheduled internal flights compared to pre-pandemic levels, with 516 new domestic routes. However, international flight numbers will miss pre-pandemic levels by nearly 30%.

Too many tourists, too little space? The backlash against overtourism and short-term rentals gathers pace

While we’ve seen incredible robustness from the global traveler, that demand has had consequences, particularly at the level of local governments.

In destinations worldwide that attract high volumes of tourists, concerns have emerged about the availability of housing and the overall impact of tourism, prompting local authorities to enact concrete legislation that requires stricter reporting and oversight of short-term rentals, as well as increases in tourism taxes and charges.

The locations where these measures are being applied highlight the fact that the increase in tourism is a major contributor to these issues, rather than just a side effect of underinvestment in housing, although that factor certainly contributes.

Italy’s tax authorities have made short-term rental incomes a focus this year, particularly from Airbnb, which a judge found had failed to collect €3.7 billion of rental income, resulting in a demand for €779.5m from the company. Florence and Venice have both announced measures to limit rentals.

In Scotland, new laws require operators to license their short-term rental property. Portugal’s government said that it won’t be issuing new licenses for vacation rentals in urban areas.

On the other side of the Atlantic, New York now requires anyone looking to make a listing of less than 30 days to register with the mayor’s office.

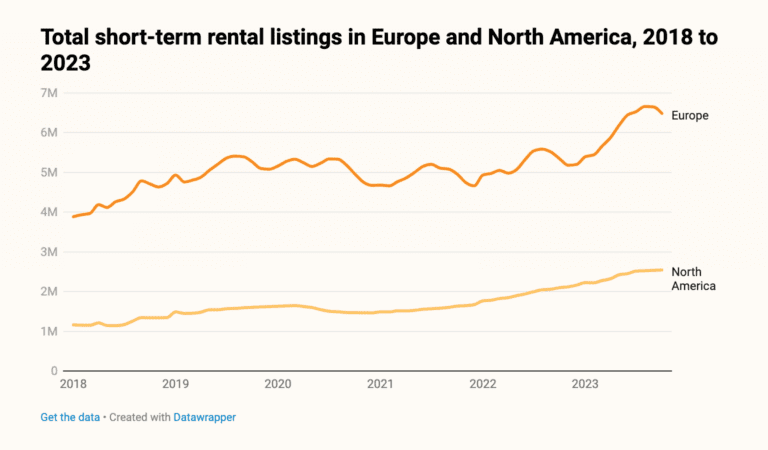

That trend reflects a remarkable expansion in the number of listings online for holiday lets, with Europe and North America leading the way. Since the start of 2018, the number of short-term rentals has grown by 40% in Europe and 54% in North America.

Our data shows there are now six-and-a-half million of these properties listed in Europe – equivalent to the total dwellings of Sweden. This has created considerable pressure on many local communities where they are most in demand.

As attempts to curb overtourism intensify, what might the potential impact be?

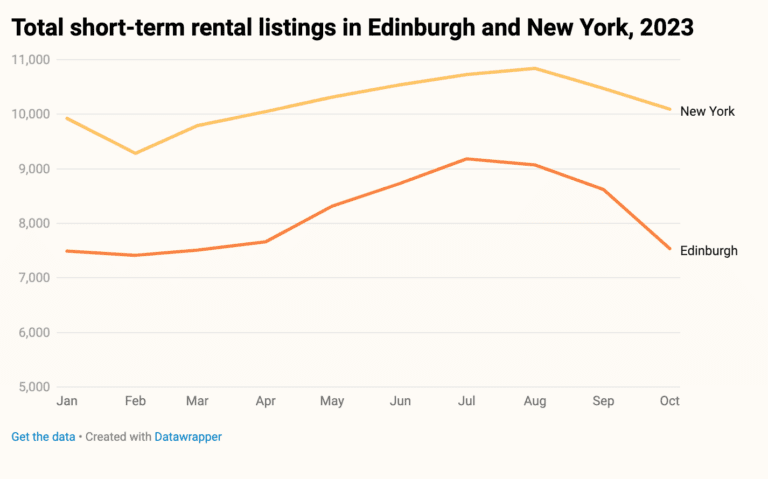

To get a clearer picture, let’s take a look at Edinburgh and New York; two destinations where there have been recent substantive changes to approach. While we are only a few short months past the legislation coming into effect, we can look at some initial data to see what may happen.

In both cases, there has been a decline in the number of listings since the measures were introduced. However, in neither case has the number of listings dropped yet to below where they were at the beginning of the year.

Meanwhile, the effect on demand and rates also seems modest. Short-term rental rates remain robust and there has been little change to hotel pricing in either city.

While overall demand did decrease slightly year-on-year in both cities in the weeks immediately after the laws came into force, it seems that travelers were not suddenly deterred.

It seems most likely, therefore, that although fighting overtourism is a rising priority, making effective legislation that creates a difference has been, and will be, challenging for local governments.

Tourists continue to want to visit these destinations and are unlikely to be keeping an eye on local bylaws. As such, a multifaceted approach is likely necessary to effectively address this issue.

The driver of technology investment in hospitality remains doing more with less

The driver of technology investment in hospitality remains doing more with less

The driver of technology investment in hospitality remains doing more with less

The driver of technology investment in hospitality remains doing more with lessOne of the reasons we have seen the robustness of travel spend noted above has been the strength of the global labor market. Unemployment in major economies continues to hover around record lows, even in the face of some economic headwinds, and vacancies are abundant.

While this means there is confidence among travelers themselves that they can rely on continued income and so make plans and bookings, the results behind the scenes of the industry are more problematic.

The travel and tourism industry shed a great deal of positions during the pandemic period, and has found it hard going to replace these workers, who have frequently moved on to other sectors.

In the UK, vacancies in the hospitality sector were 72% higher in Q1 2023 compared to Q1 2020, and those levels have remained consistent throughout the year. Or in the US, despite employment rates now edging back to pre-pandemic highs, 87% of hotels said that they could not fill their open positions according to the American Hotel & Lodging Association (AHLA), continuing a trend of difficulty in hiring going back several years now.

That dynamic is pushing a drive for more automation across hospitality, both in the front- and back-of-house, as almost all organizations are now forced to do more with less.

Contactless was key in 2023

While the front-of-house for hotels is always going to require a human face, automation is making increasing inroads, especially as key workers like cleaners, cooks and concierges become scarcer and more costly.

Machines clearly can’t do all these tasks, but we are seeing more deployments of systems like cleaning robots and smartphone integrations to help reduce the workload of hotel staff.

We saw these systems proliferate in 2023 because of the dynamics explained above, but also because the consumer is heading that way in terms of behavior, making this one to watch going forward as well.

An increasing number of travelers not only accept and use contactless forms of interaction, with the pandemic accelerating this, but also want to utilize these systems, finding them (if done well) convenient and less hassle than calling or heading down to the front desk.

Critically for hotels, this is another route into the consumer’s digital presence and potentially owning the relationship with the customer, giving this trend impetus from both directions.

Now there is a compelling reason for guests to interact directly with the hotel and download an app, through which hotels can market and sell ancillaries, improving both guest experience and revenues, while reducing staff workloads.

Therefore, expect to see a whole lot more machine-to-man integrations in hotel lobbies in the near future.

Hoteliers move into the automation age

It’s not just on the frontline where smaller teams have become the norm, as white-collar workers are also having to get used to smaller teams. This has made software-as-a-service tools invaluable across the industry as critical time-savers in 2023 for revenue, general, marketing and sales managers.

The increasing ability to plug-and-play these services supercharged the market in 2023 and now we are seeing analytical and management tools becoming the norm, and a decline in the old spreadsheet-dominated model of hotel management.

Their rise rests on their ability to increase productivity, which as we have noted is critical in this environment. A revenue manager can now utilize a single commercial platform to visualize market demand, analyze competitor behavior and pricing, look at booking curves, monitor rate parity, set rates, benchmark and then communicate this with the wider management team.

This is a game-changer for these teams, within many common tasks reduced down to a fraction of what they once were, and can turn an imbalanced workload in the post-pandemic years into a much more manageable set of tasks.

Generative AI makes inroads into the hospitality industry

If you haven’t used ChatGPT to form a travel itinerary yet, then you should check it out. For example, if you prompt it to create a five-day travel itinerary for Kyoto, Japan, it not only will correctly identify key sites, but structure that itinerary in a (largely) thematically and geographically cogent way that would rival a guidebook. Is this the future of travel planning? Well, we can’t say for sure, but it’s going to be a resource travelers use in the future.

The industry needs to be aware of its power and potential from this side, but also what generative AI integrations might mean for their own brands and customer interactions.

We’ve already seen the rise of chatbots within the travel sphere to help with basic queries and direct guests, but this offers a step-up in capability, allowing far more freedom for the customer to ask questions in their own way and to get to the right answer.

Now, a chatbot integration can answer more queries independently and also bring in a vastly wider corpus of knowledge to help the guest. Leveraging AI-powered smart room technology can also enhance your guests’ experience while maximizing maintenance efficiency and managing energy usage.

You can streamline your demand forecasting phase by using predictive analytics to generate demand predictions quickly and accurately. Our Market Insight solution, powered by unique AI demand segmentation technology, turns forward-looking search data points into real-time demand levels, providing you with valuable market intelligence broken down by sub-location, stay pattern, and hotel type.

AI brings unique opportunities for revenue managers that don’t just stop at demand forecasting. If paired with the right data sets, we will see an impact on revenue strategy compared to traditional price recommendation algorithms. Revenue managers will be able to capture every revenue opportunity automatically, as room pricing adjusts in real-time with AI-driven recommendations.

Summary

Despite concerns over economic conditions, such as rising inflation and interest rates, the desire to travel has remained strong in 2023 and there should be an overall feeling of positivity.

The continued drive for in-person experiences has led to a surge in demand for major sporting, cultural, and music events, and, as a result, has been a huge demand driver for hotel and short-term rental bookings. Business travel has also made a comeback, with expenditures rapidly approaching pre-pandemic levels.

Additionally, the hotel industry is also turning to automation, machine learning and generative AI which is offering unique opportunities for hospitality professionals.

In order to optimize performance, to ensure you get ahead of your peers rather than play catch up you should look to a full circle commercial platform powered by quality data, which takes care of everything from demand forecasting and AI pricing recommendations to benchmarking against your Comp Set.