In the past 5 years, the restaurant technology landscape has seen significant expansion and diversification with great effect on the business of running restaurants. On the back of huge growth in cloud and mobile technology, as well as the global adoption of consumer tech in general, operators are embracing and seeing the value in, technology at almost all levels of the stack in both guest experience (B2C), and operations (B2B).

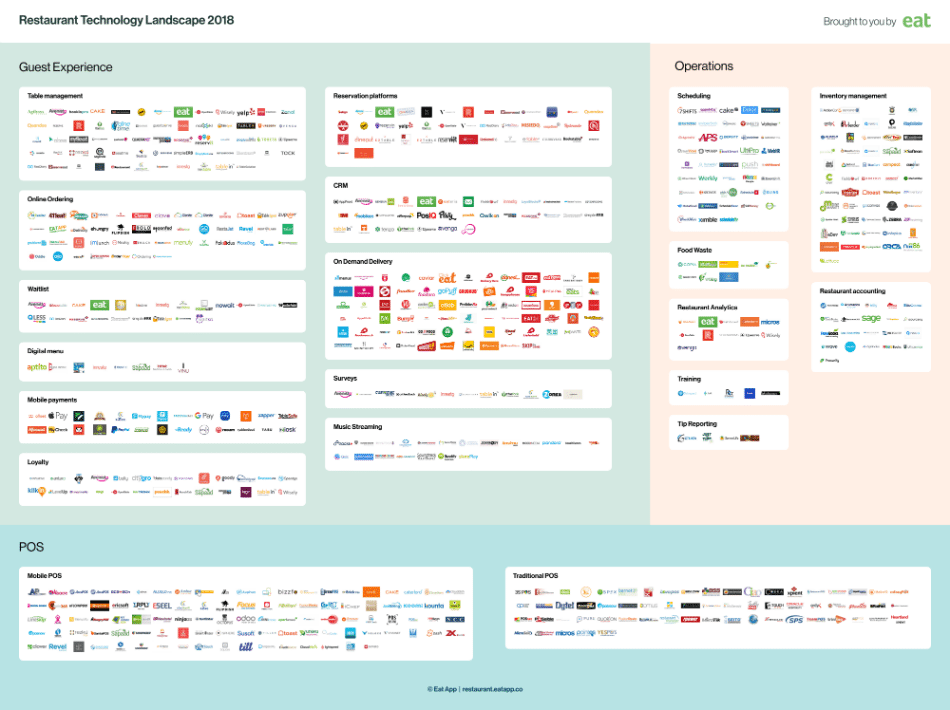

This infographic aims to provide anyone with interest in the restaurant industry, a complete snapshot of the restaurant technology stack in 2018. Download a high-resolution version. (Google Drive link)

This infographic aims to provide anyone with interest in the restaurant industry, a complete snapshot of the restaurant technology stack in 2018. Download a high-resolution version. (Google Drive link)

The move to digitization in the entire restaurant value chain has ushered in a new era for operators where customer data sits at the heart of decision making. Today, increasingly sophisticated reservation systems are replacing pen and paper and providing access to entirely new reservation markets. On-premise POS systems are giving way to synced tablets offering data sharing APIs, and the dramatic rise of on-demand delivery is causing some restaurants to re-think their entire revenue strategy.

While, as an industry, we can see anecdotally shifts taking place, it is hard to get perspective on what this actually looks like in reality. In response, we felt it would be helpful to visualize a complete picture of the restaurant technology landscape to get a sense of which parts of the value chain are seeing the most disruption and competition, as well get an overall sense of the size of this sector.

Three main themes were apparent with the existing material available on the restaurant tech landscape.

- Existing mappings of this type are usually illustrative rather than comprehensive and don’t tend to give an accurate representation of a sheer number of companies competing in this space. These are great for understanding where tech providers are adding value but don’t give a sense of the size of each sector.

- Some have looked at what might be called the ‘Foodtech’ landscape, which takes into account everything from recipe services and grocery delivery to restaurants. We wanted to focus specifically on restaurants which are a better-defined ecosystem.

- Previous attempts to chart the landscape tend to focus on US companies when in reality the competitive landscape is in fact much more global with some of the largest restaurant tech platforms now based in China.

Let’s take a look at some of the key takeaways:

On-demand delivery is the biggest market in B2C

In the consumer-facing space, on-demand food delivery is most well-represented category globally with new players continually entering the market. Analysis of in venture capital investment in the restaurant space by F Prime Capital shows why the delivery market now represents the largest slice of the B2C pie.

3rd Party platforms vs white label solutions in the delivery and reservation space

Whilst most of the media coverage is around how 3rd party reservation and delivery platforms are continuing to amass millions of loyal users through high consumer demand, optimized logistics and network effects, there are also a significant number of SaaS table management and delivery solutions helping restaurants tap into these channels without paying the margin-destroying fees of the large consumer platforms.

Traditional POS is still a major category

POS is by far the biggest technology category in the restaurant business. POS has changed a lot in the past 5 years with the shift to cloud and mobile with many restaurants switching to modern and more flexible products. But there at least 15 million restaurants in the world and not everyone has made the switch. Traditional, on-premise POS companies rival their newer competitors in numbers.

Notes on Restaurant Technology Landscape infographic

We used a combination of online tools for the research including Google and software aggregators like Capterra. Although we tried, any project like this can’t ever hope to be 100% exhaustive. We aim for this to be an ongoing project that develops over time so if you have feedback or think we’ve missed any companies please let us know here.

We split the landscape into 3 main categories. Guest Experience, POS and Operations. The design is laid out so that POS straddles both guest experience and operations suggesting that as the ecosystem develops, POS systems are sharing data between both front and back of house functions.