U.S. hotel performance for the week ending Aug. 28 reflected seasonal trends as well as the continued impact of the pandemic on business travel, and it’s too soon to see any significant effects of Hurricane Ida among hotel numbers in markets affected by the storm.

U.S. hotel performance for the week ending Aug. 28 reflected seasonal trends as well as the continued impact of the pandemic on business travel, and it’s too soon to see any significant effects of Hurricane Ida among hotel numbers in markets affected by the storm.

Occupancy fell by more than two percentage points to 61% for the week. This was the fifth consecutive week with lower occupancy and the fourth straight week with an occupancy decline of more than two percentage points.

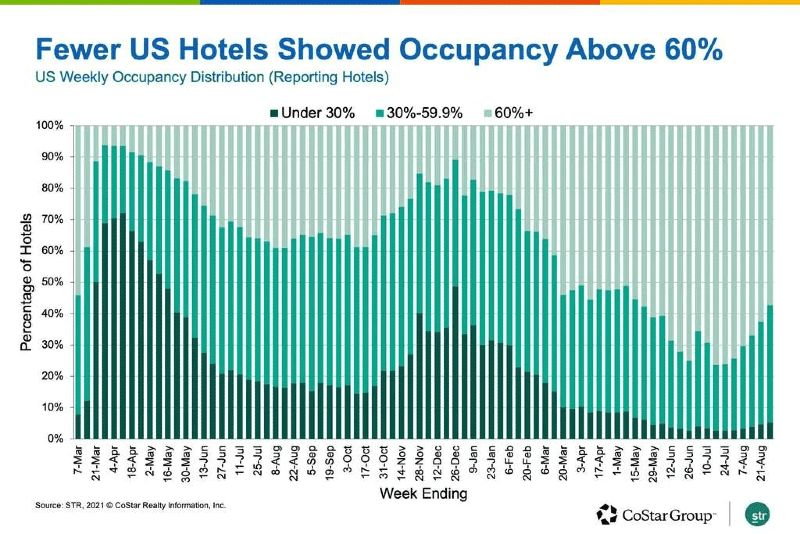

More than 77% of all STR-defined markets in the U.S. reported lower weekly occupancy, and U.S. occupancy is now at its lowest level since mid-May as just 57% of hotels saw weekly occupancy above 60% — the lowest percentage in 14 weeks. Weekday and weekend occupancy have each been trending down for the past five weeks.

On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, weekly occupancy was 58.8%. In the U.S., there are still 49,000 rooms closed, 40% of which are in New York and Orlando.

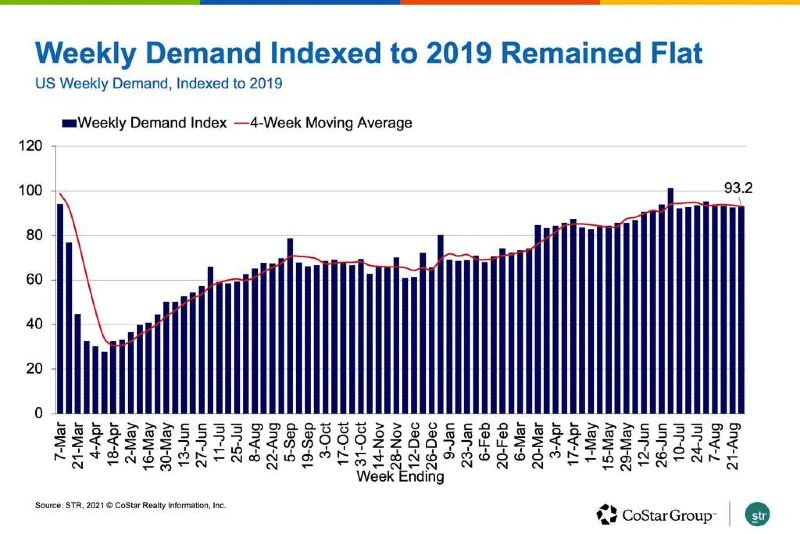

At 23.6 million room nights, weekly room demand was the country’s lowest since early June and 93% of what it was in the comparable week of 2019. At the same time, the demand index to 2019 increased 0.8 points week on week because of the shift in the Labor Day holiday, which began at the end of the corresponding week in 2019. Daily demand indices showed a general rise across all days, particularly midweek, as 2019 business and group travel slowed ahead of the holiday.

For the past 12 weeks, room demand has been 90% or more of the comparable 2019 level. However, we expect it to soften further as leisure travel pauses given the resumption of in-person schools, increased anxiety from the Delta variant surge and limited business travel.

Taking a closer look, room demand fell the most in Florida with Orlando and Miami accounting for more than half of the state’s loss. Among other states, Louisiana’s room demand rose slightly over the weekend ahead of Hurricane Ida. Texas, Alabama and Georgia also saw growth over the weekend. STR will produce more thorough analysis on the Ida impact on performance and closures in future weeks. Overall, only six states saw demand grow week over week, led by Massachusetts. And while there is noise due to the Labor Day holiday shift, it is worth noting that 14 states still reported weekly demand greater than what it was in 2019, down from 18 in the previous week.

Next week’s data is expected to see wider market-level variations due to this year’s Labor Day holiday along with the impacts of Hurricane Ida from Louisiana to the Northeast. While all notable key performance indicators are falling, we don’t expect a fall to the levels seen earlier this year. TSA screenings, while down from their leisure highs, continue to be better than 70% of the levels they were in 2019. Of course, only time will tell.

Absolute average daily rate (ADR) was $132, a 10-week low and down 3% week on week, which was the largest weekly decrease since mid-April. Overall, ADR has come in lower for four straight weeks, and when indexed to 2019, the metric was down two points to 103% — meaning ADR was 3% higher than what it was in the comparable week of 2019. The decrease in the index was the steepest of the past two weeks.

Despite the fall in the index, more than 130 markets (78%) continued to report ADR that was higher than 2019 on a nominal basis. The number of markets observing higher nominal ADR than in 2019 has shown little change over the past five weeks. Eighty-eight markets reported real ADR—adjusted for inflation—higher than what it was in 2019, down from 103 markets a week ago. Overall, U.S. weekly real ADR was at 98%, down two points from the previous week.

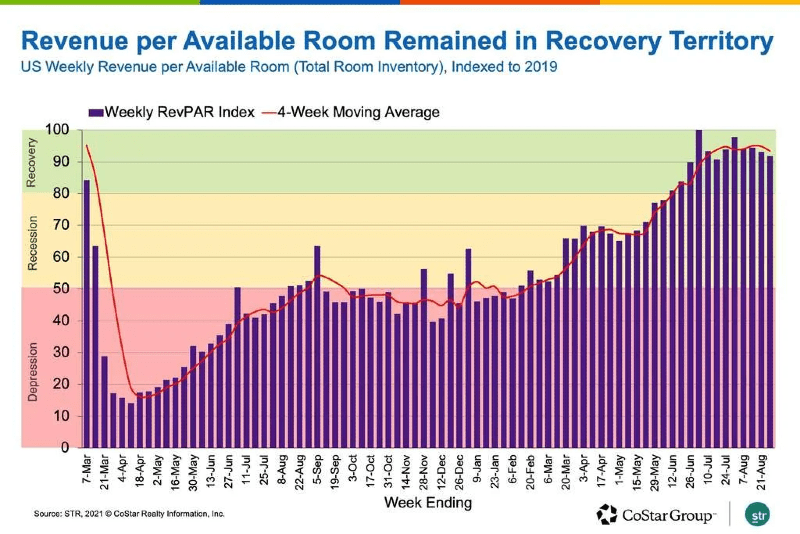

Revenue per available room (RevPAR) on a total-room-inventory basis declined 7.2% week on week to $78, which was the largest decrease in 19 weeks and the lowest absolute total-room-inventory RevPAR in 12 weeks. Indexed to 2019, nominal total-room-inventory RevPAR was 92%, down 1.3 points week on week and the second consecutive weekly decrease. Real total-room-inventory RevPAR indexed at 87%.

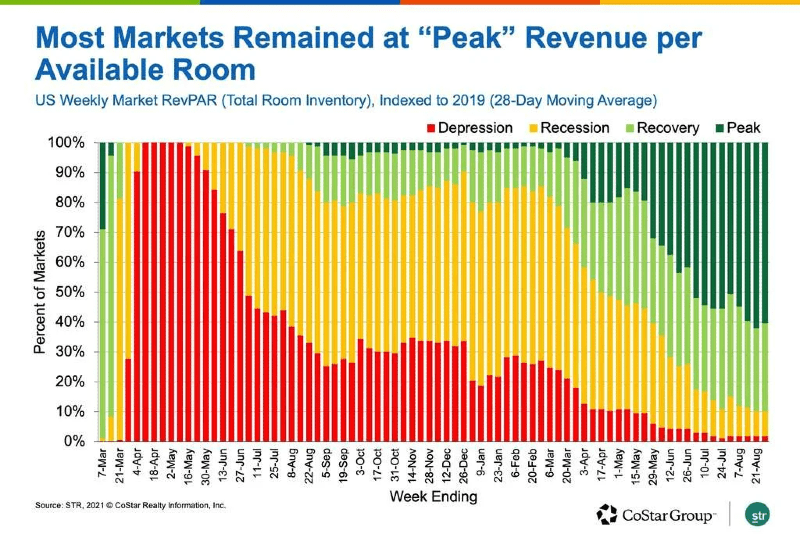

On a 28-day moving total basis, total-room-inventory RevPAR indexed to 2019 dropped to 88% after coming in at 90% a week ago but remained in STR’s “recovery” category as it was above 80. On a market-level, 100 markets had nominal total-room-inventory RevPAR at “peak,” meaning it was above the level seen in the comparable 2019 week. A week ago, 103 were at “peak” levels, which was the most so far. Seventeen markets remained in either “depression” — total-room-inventory RevPAR indexed to 2019 under 50% — or “recession” — total-room-inventory RevPAR indexed to 2019 between 50% and 80%. The remaining markets (49) were in “recovery.”