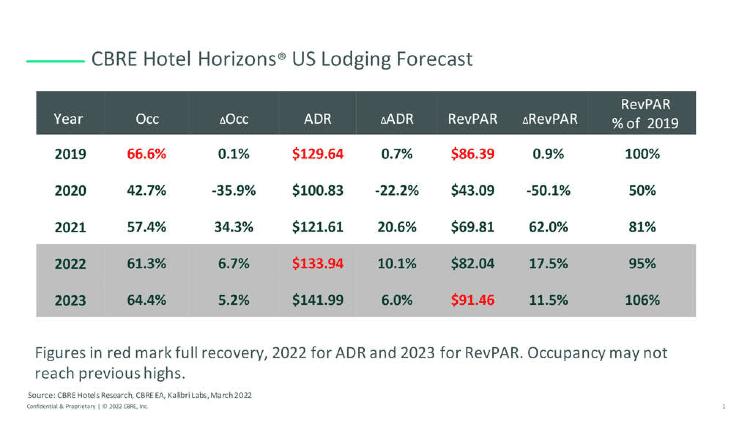

CBRE Hotels Research has raised its forecast for 2022 average daily rate (ADR), Occupancy and Revenue per available room (RevPAR) to reflect the stronger-than-expected fundamental performance in the fourth quarter.

CBRE Hotels Research has raised its forecast for 2022 average daily rate (ADR), Occupancy and Revenue per available room (RevPAR) to reflect the stronger-than-expected fundamental performance in the fourth quarter.

Other factors contributing to the improvement include below-average supply growth, strong domestic leisure trends, the resumption of inbound international travel, and a predicted return to office later this year. CBRE made the changes despite heightened uncertainty and increasingly limited visibility due to geopolitical risks and inflationary pressure.

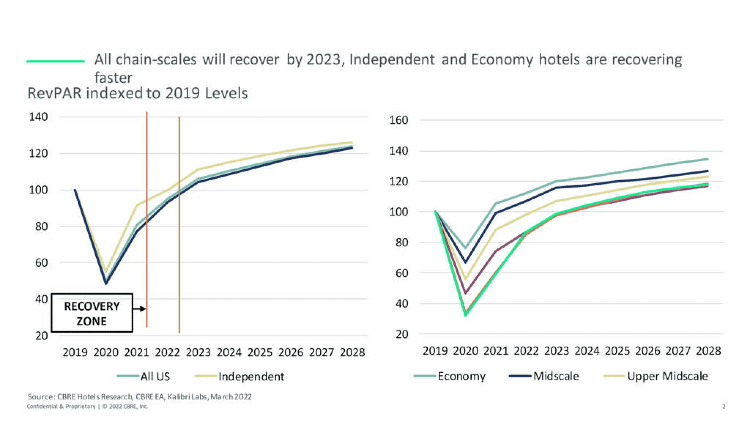

CBRE now forecasts RevPAR to reach 2019 nominal levels by Q3 2022 under CBRE’s base case scenario, rather than in Q3 2023, as previously forecasted.

RevPAR in December 2021 exceeded 2019’s levels for the first time since the pandemic began. This strength has not held into this year’s first quarter. January saw a pullback, with RevPAR coming in 21.7 percent below 2019, and year-to-date trends have remained somewhat muted. The pullback is likely due to the shift from the leisure-centric holiday season to the business-driven first quarter along with heightened geopolitical and inflation risks.

According to CBRE Hotels Research’s December 2021 edition of its Hotel Horizons report, ADR reached 2019 nominal levels in last year’s third quarter. CBRE expects that ADR will once again exceed 2019’s levels following a pause this quarter. Higher rates will be driven by a recovery in higher-rated, inbound international travel, the resumption of more traditional business travel, labor market tightness and higher overall inflation. US CPI was 6.7 percent year-over-year in Q4 2021 and hit 7.9 percent in February 2022, according to the Bureau of Labor Statistics. CBRE forecasts that inflation (CPI) will reach slightly more than 6 percent in 2022 before dropping to around 2 percent in 2023 and after.

“Higher room rates will lead to a quicker return to 2019’s nominal ADR levels,” said Rachael Rothman, CBRE’s Head of Hotel Research & Data Analytics. “But from a profitability perspective, inflation will be a headwind through higher utilities, supplies and labor.”

The effects of inflation on ADR won’t be uniform. Bram Gallagher, CBRE Senior Hotel Economist said, “Historically, most hotels can respond to inflation with price increases, but only luxury hotels have demonstrated that they can exceed the pace of inflation to achieve real gains. Economy hotels have the most difficulty raising prices enough to keep up.”

CBRE expects domestic and drive-to resorts to show strength once again in 2022 as the war in Ukraine and the resurgence of COVID in Asia could persuade wealthier US travelers to prefer domestic destinations closer to home. Elevated gas prices could hurt more budget-minded consumers who frequent interstate hotels.

Longer-term, muted supply growth will mitigate the blow for the hotel industry. High construction-material prices, including lumber, steel, and labor, make the development of most new projects cost-prohibitive, limiting the delivery of new rooms over the medium to longer term. CBRE forecasts that supply will increase at a 1.2 percent compound annual growth rate over the next five years, well below the industry’s 1.8 percent long-term historical average.